Source: Canada’s Venture Capital Landscape Report (2023) — BDC

Objective

The venture capital landscape is a dynamic and ever-evolving environment, where success is measured not only by achieving high valuations but also by generating strong returns for investors. As we saw companies climb Mount Everest to unicorn statuses in the past 18 months, many failed to get back down safely to survive.

It is imperative for Canada to ensure transparency in venture capital returns to remain globally competitive. Open dialogues on challenges and strategies are part of this effort. The aim is to disseminate insights, equip other fund managers with valuable knowledge, and bolster Canada’s standing in the global venture capital sphere. This collective effort has the potential to drive Canadian startups forward and attract international capital and talent to this burgeoning ecosystem.

In Canada, the federal government has been influential in creating a conducive environment for startups and venture capital, through initiatives such as the Business Development Bank of Canada (BDC) and the Venture Capital Catalyst Initiative (VCCI). These efforts have proven crucial in supplying public funding to draw in private sector capital and kickstart the Canadian VC ecosystem. The significant contribution of these programs in laying the groundwork for a sustainable and competitive startup ecosystem globally is acknowledged and appreciated. Without such support, a number of companies and funds could face substantial hurdles in launching and realizing their full potential. The federal government’s dedication to fostering innovation and entrepreneurship has played a major role in developing the Canadian startup ecosystem.

The 2023 Venture Capital Landscape Report by BDC revealed data on Distribution to Paid-In capital (DPI) Across Vintages, indicating that the upper quartile of Canadian funds from pre-2011 to 2013 recorded a 1.2x DPI. This contrasts with the 2.0x DPI of U.S. incumbent funds during the same period, as reported by Cambridge Associates. This difference illustrates the distinct market dynamics that characterized the less mature Canadian venture capital sector during this time. However, since then, Canada’s ecosystem has seen substantial growth, reflected in an increased number of venture funds and startups, and overall improved performance. Notably, most of the active venture funds in Canada, including Ripple Ventures, have been established in the past 5–7 years, underlining the recency of this expansion.

While we acknowledge that not all venture capital funds wind down after the traditional 10-year period and extensions can occur, a strategy that funds can take to protect the performance over the life of the fund is to return at least the original capital within the first 6–7 years. This approach allows for sufficient time and opportunities to graduate the portfolio and reduce the entire reliance on unpredictable outliers of breakout companies alone to return the fund. This strategy increases the chances of moving from a 1x to 3x+ return within the remaining 3–5 years.

As such, we want to cover two general approaches to achieving a 3x fund. The first relies solely on 1–2 outlier investments that generate significant returns in the final years while having minimal returns in the earlier stages. The second approach involves consistently returning capital throughout the fund’s lifecycle, allowing the mediocre outcomes to return the original capital and for the winners to drive true profit. We believe that the latter approach is more sustainable and favorable.

While the former approach can be challenging, requiring a consistent scale of exits and various factors to align perfectly, our belief is that consistent capital returns across the portfolio create a higher probability to outperform over the long run. At Ripple, we personally invest a significant portion of our net worth into our funds, making us very aligned with our limited partners to strive not only for homerun outcomes but also to return our own original investment.

Our goal is to open up the discussion of fund performance, key drivers of winning strategies, and how we can put Canada as a winner on the global stage. By highlighting benchmarks and sharing insights from our journey, we aim to contribute to the broader conversation about driving enterprise value in Canada. We recognize the importance of collaboration and knowledge-sharing in building a strong ecosystem, and we are committed to playing our part in its development.

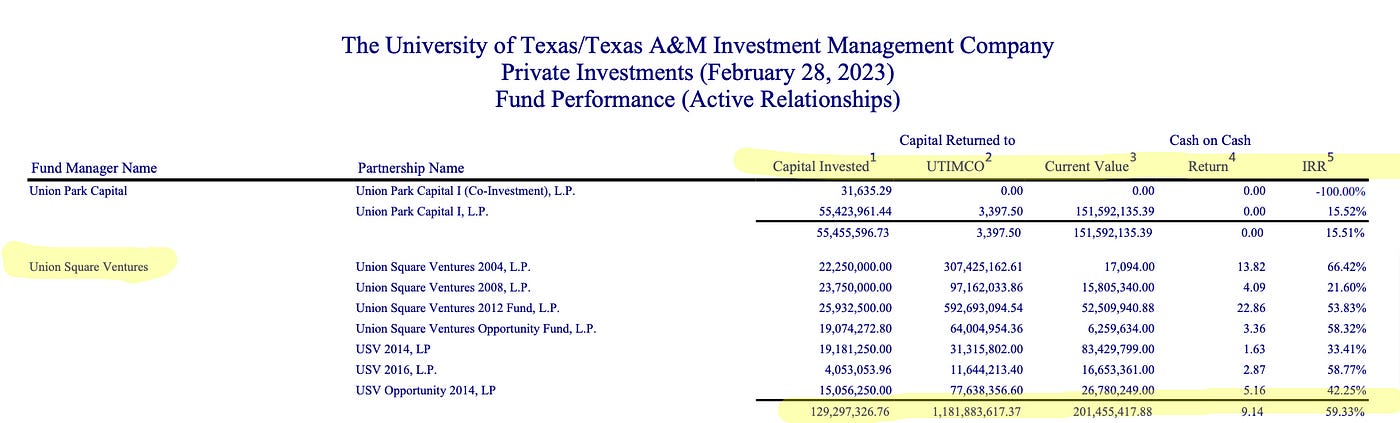

Union Square Ventures — the gold standard for DPI

Before diving into the details, we want to establish the gold standard DPI benchmark that every fund should strive to achieve. Recent returns data from the University of Texas Endowment, as highlighted by Eric Newcomer’s blog, has captured attention. Union Square Ventures has demonstrated exceptional performance, delivering 9x DPI cumulatively across all their funds. Their 2012 vintage fund, with a DPI of nearly 23x, stands as one of the best-performing funds of all time. These extraordinary returns showcase Union Square Ventures’ track record of staying focused on key themes, investing only with high conviction, acquiring material ownership, and keeping fund sizes small to be able to consistently return capital to LPs.

Source: University of Texas

Ripple’s DPI performance relative to incumbents

Ripple Ventures has established an early track record in our angel portfolio since 2012 (we call this Fund 0) currently at 6.5x DPI. Although Fund 0 was an angel portfolio with a smaller quantum of capital (which is easier to return), it is worth noting that our success is not solely reliant on one outlier investment to drive strong returns. Instead, we have strategically managed a portfolio including three of ten investments achieving at least 10x cash-on-cash returns (with the highest returning 30X). We have personally recycled a majority of this capital to jumpstart Fund I and attract external limited partner capital for our venture funds.

We continue to build on our track record with Fund I (2019 Vintage) with a DPI of 0.5x. Again, Fund I was also a smaller fund compared to most at $10M which makes it much easier to return than a $200M fund like USV’s. Considering the limited maturity of the 2019 vintage, it is important to acknowledge the current challenging market cycle and the pressure for funds to generate significant returns despite the bleak outlook for exits in the near future. As we approach the halfway mark of the fund’s life, if the original capital has not yet been closer to being returned, there is still a long hard way to achieve a 3x+ DPI.

When comparing to US incumbents, upper quartile returns were: 2.61x DPI (2011), 1.90x DPI (2012), and 1.48x DPI (2013) respectively according to the latest US Venture Captial return reports. The average DPI across the 2011–2013 vintage is 2.00x DPI, 67% higher than its Canadian counterparts. There is a stark difference between the median performance of top quartile funds in Canada vs the US. In the 2019 vintage, Ripple Ventures is categorized in the top 5% of funds based on DPI in the US so far.

While Ripple Ventures Fund I is still in its early stages and hasn’t achieved a 3x+ return yet, we approach this journey with humility, dedication, and empathy. We understand the uncertainties of the venture capital landscape and the possibility that we don’t continue to exceed expectations. However, we are committed to diligently managing our portfolio, making informed decisions, and striving to deliver exceptional returns. With transparency and empathy at our core, we will continue to navigate the evolving market dynamics to create long-term value for our investors.

Our view on what drives DPI, and differences in Canada vs the US

Ownership and exit value play crucial roles as the primary drivers of DPI in venture capital funds. You need to have at least one or the other to drive returns, and in the best cases, you have both. For example, if you have a $50M fund, you need to own 20% of a $250M exit, or 1% of a $5B exit to return the fund ($50M). Let’s take a look at another graph in the BDC report around median exit values to understand better why DPI may be different in Canada vs the US:

Source: Canada’s Venture Capital Landscape Report (2023) — BDC

You can see there’s a very evident difference in the historic outcomes of companies in each country. According to PitchBook, the average exit value for US venture-backed startups was approximately $207M USD in 2019, $263M USD in 2020, and $391M USD in 2021. These are multiples higher than the Canadian counterparts.

Although this is the case, we want to acknowledge the potential for creating global winners in Canada, such as Shopify and Lightspeed (public companies), as well as notable private outcomes like Wattpad’s acquisition by Naver for 754 million CAD and Verafin’s sale to Nasdaq for 2.75 billion USD in cash. It is crucial to highlight the potential for Canada to create companies of this scale, but recognize the lower frequency in which this occurs. By learning from and comparing ourselves to the best in the world, particularly the United States, we can identify the strategies and practices that contribute to their success.

Why Ripple is investing in both Canada and the US

Ripple Ventures recognizes the tremendous potential of the Canadian startup ecosystem and aims to drive enterprise value creation for early-stage companies by leveraging the expertise and resources from the US network. We firmly believe that adopting a strategic investment strategy that spans Canada and the United States is essential for the success of fund managers seeking to achieve 3x+ DPI. Our approach is driven by the objective of bringing valuable knowledge, networks, and resources from the US ecosystem into Canada, accelerating growth, and fostering better returns.

In Canada, there is a shortage of founders and employees who have experienced the journey from idea to IPO, hindering the mass development of unicorn companies we’ve seen in the US. By investing across borders, Ripple Ventures facilitates the exchange of knowledge and experience, allowing Canadian founders to tap into a wealth of resources and navigate the challenging “valley of death” stage. This exposure to higher-scale ventures and outcomes creates a fertile ground for innovation, fueling the growth of early-stage companies.

We firmly believe that bridging the gap between the Canadian and US ecosystems is pivotal in driving higher enterprise value exits. Currently, Canada only has 25 unicorns generated compared to the US in which there are 700+, and we aim to change that narrative. It must be stressed that investing in Canada today can still be an extremely profitable venture, but this hinges greatly on the degree of ownership an investor can secure. Given the historical performances, a high ownership stake is a significant factor that can help offset the inherent risks and volatility of the scale of venture capital outcomes in Canada.

Ripple Ventures is committed to being at the forefront of driving the next generation of category-defining companies in Canada. By leveraging our connections, networks, and experiences from both sides of the border, we aim to catalyze the growth of the Canadian startup ecosystem and pave the way for greater success. If you don’t believe us, just ask our founders if we have been successful at doing this.

Why keeping fund size smaller matters

Keeping fund sizes smaller is a strategic choice that aligns with Ripple Ventures’ investment approach and objectives. It allows us to focus on specific stages, check sizes, ownership targets, and industries that fit our investment thesis. By maintaining smaller funds, we prioritize efficient capital deployment and maximize our ability to generate significant returns for our investors. This approach is particularly advantageous when considering the quantum of exit size relative to the respective market and entry stage.

We’ve seen USV consistently keep their fund sizes relatively the same in all market environments because their formula works. In our view, the game of venture fund managers should be to execute the strategy that you know works for generating strong returns for LPs and raising/recycling capital to keep it going over multiple funds. At Ripple, we’ve made a commitment to our LPs that we’d never scale the fund past a size that makes sense and is possible to outperform (3x+ DPI). If it ain’t broke, don’t fix it.

Ripple’s philosophy in portfolio construction to drive DPI

Ripple Ventures adopts a strategic approach by investing across both Canada and the US, employing a barbell strategy to optimize returns within each fund. Recognizing the historical disparity in exit values between the two markets, we tailor our investment strategy accordingly.

In Canada, where exits have traditionally been lower, the focus is on playing the ownership game. By securing substantial ownership stakes in companies, Ripple Ventures ensures that even in more modest exits, the ownership-driven returns can generate significant DPI for the fund.

Conversely, in the US market, where valuations are higher and obtaining ownership can be more challenging, Ripple Ventures is willing to trade off lower valuations. This balanced approach allows us to capture the potential for higher exit values and drive DPI.

In our opinion, employing a barbell strategy is essential for fund managers in Canada to ensure that the interplay between ownership and exit scale is thoughtfully priced into their portfolio, maximizing returns and achieving their target of surpassing the gold standard of 3x DPI.

At Ripple Ventures, we deeply admire and draw inspiration from funds like Version One Ventures and Golden Ventures, who have successfully executed the strategy of investing across North America &globally while being based in Canada. These funds serve as valuable partners within the Canadian ecosystem, bringing exposure to top-tier founders, operators, and investors from the US. Their ability to connect with and learn from the best in the industry helps them level up not only their own expertise but also their portfolio companies. We share a common goal with these funds — to drive growth, foster innovation, and create a thriving startup ecosystem in Canada by leveraging the insights and resources available across North America.

Conclusion

Our ultimate aspiration at Ripple Ventures is to become the Union Square Ventures of Canada, driving the best-returning fund out of the country. Merely returning the original investment would be considered a failure for us. That’s why we are igniting this conversation and delving into the intricacies of our strategy.

By focusing on early-stage investments, prioritizing ownership, investing across both Canada and the US, and actively driving DPI throughout the entire life of the fund, we are positioning ourselves for a higher probability of achieving our goal of becoming a globally recognized and outperforming fund.

Transparency in venture capital returns is crucial for Canada to compete on a global scale. By openly discussing challenges and strategies, we aim to elevate the industry and drive meaningful conversations. Our goal is to share insights, empower other fund managers, and strengthen Canada’s position in the global venture capital landscape.

Get in touch:

Matt Cohen, Managing Partner at Ripple Ventures (matt@rippleventures)

Dominic Lau, Partner at Ripple Ventures (dom@rippleventures.com)

Share this post